Debt portfolio structure

On the path to change

All our borrowings are free of collateral or other security, which is a sign of the high level of trust investors have in the Company. The share of public debt instruments stood at 100% at the end of the year.

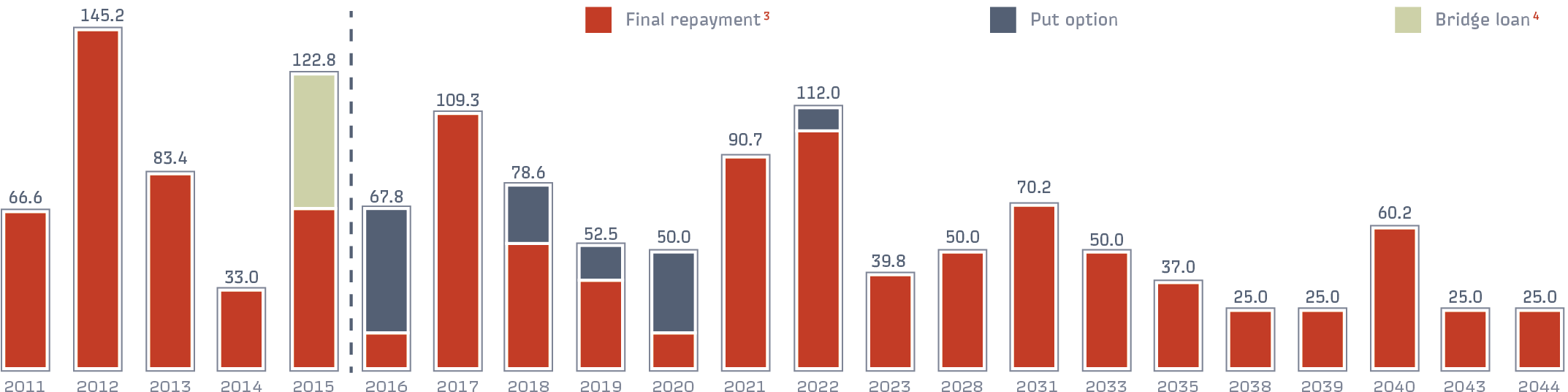

The total amount of debt is contained within the limits of the debt policy. The share of short-term borrowing was only 7% at the end of the year, a decrease of 8 p.p. from the previous year’s level. The repayment schedule is balanced for the long term, which minimises refinancing risks.

The debt load of the Russian Railways Group is at a comfortable level: the net debt/EBITDA ratio was 2.32x as of 31 December 2015 (per IFRS) compared with 2.37x on 31 December 2014.

Based on materials from the final meeting of the Russian Railways Management Board

The Company takes a balanced approach to managing its loan portfolio and attracting debt capital while also ensuring the necessary funding for strategically important infrastructure projects with a long payback period and flexibility in the management of current liquidity taking into account the specifics of business.

Russian Railways borrowed a total of RUB 158.3 bln in credit funds in 2015, including:

- RUB 97.2 bln from infrastructure bonds;

- RUB 45 bln in form of exchange bonds;

- RUB 16.1 bln as part of a second placement of Russian Railways bonds previously purchased in an offer.

Russian Railways repaid RUB 122.8 bln in loan obligations in the reporting year.

The Company attracted bilateral bank loans throughout 2015 for the day-to-day management of liquidity in the amount of RUB 128.8 bln, which it had fully repaid as of 31 December 2015.

The overall debt portfolio (including exchange rate fluctuations) exceeded the 2014 level by RUB 132.7 bln as of the end of 2015 and amounted to RUB 988.9 bln (the debt portfolio amounted to RUB 969.2 bln excluding accrued interest payable).

The growth in the loan portfolio is mainly attributable to the significant depreciation of the rouble throughout 2015, which led to the revaluation of foreign currency-denominated obligations (influence: RUB 91 bln).

The long-term portion of the loan portfolio (maturity of more than 3 years) increased to 74% as of the end of 2015. The 7.5% increase (year-on-year) in the portion of long-term obligations in the loan portfolio is related to funding acquired for investment projects with long payback periods (over 20 years) that are typical for the industry, as well as the repayment of short-term borrowings the Company received in late 2014.

The share of medium-term borrowings with repayment periods ranging from 1 year to 3 years remained unchanged compared with 2014 at 19%, while the share of borrowings with repayment periods of less than 1 year declined significantly to 7%.

The average maturity of liabilities in the loan portfolio was approximately 10 years as of the end of 2015. The debt repayment schedule ensures the even distribution of payments over the long term and minimises risks associated with refinancing. The largest single debt maturity denominated in foreign currency is planned for the early second quarter of 2017.

In terms of instruments, the Company maintained the diversified structure of its loan portfolio in 2015 with a focus on public instruments. The share of infrastructure bonds increased from 24% to 31%, which is attributable to the placement of 6 additional issues of these bonds for a total of RUB 97.2 bln for a period ranging from 15 to 30 years at a rate tied to the inflation level.

In the past, Vnesheconombank had been the sole investor in this type of security, however in 2015 the infrastructure bonds were also purchased using money from the National Wealth Fund, which bought RUB 60.2 bln worth of bonds.

The proportion of rouble-denominated borrowings in the Russian Railways loan portfolio decreased in 2015 due to the significant impact from the revaluation of borrowings denominated in foreign currency and stood at approximately 54% as of the end of 2015, which is 6% lower than the target set by the Company. However, the long-term debt portfolio management policy remains unchanged in terms of maintaining the rouble-denominated portion of the portfolio at a level close to 60%. In this regard, Russian Railways management is taking steps to reduce the proportion of foreign currency-denominated borrowings, including through their partial refinancing using rouble-denominated instruments. In particular, foreign currency-denominated obligations for a total of EUR 125 mln were repaid in late 2015.